In recent years, Buy Now, Pay Later (BNPL) services have become one of the fastest-growing trends in finance technology, offering consumers an alternative way to shop without using credit cards. With companies like Klarna, Afterpay, Affirm, and PayPal’s Pay-in-4 becoming mainstream, BNPL has reshaped how people, especially younger shoppers pay for everyday purchases.

But is BNPL truly a convenient financial tool, or is it quietly pushing consumers into debt?

Let’s break it down.

What Is BNPL and How It Works

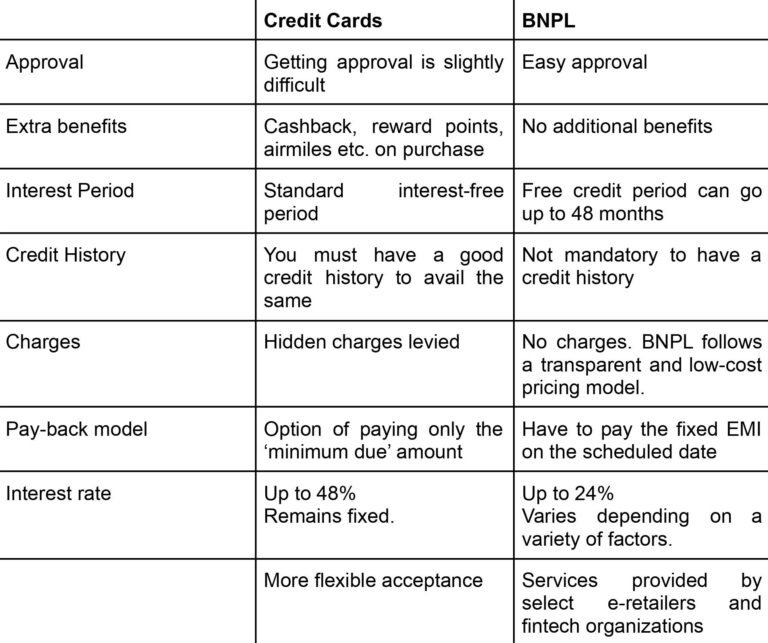

BNPL is a short-term financing option that allows shoppers to split payments into smaller installments, often interest-free.

The typical flow looks like this:

- Choose a BNPL option at checkout

- Pay a small portion upfront (usually 25%)

- Pay remaining installments over weeks or months

- No interest, unless a payment is late

- Soft credit checks or no credit checks at all

This seamless experience powered by modern finance technology has made BNPL extremely popular across e-commerce, travel, healthcare, and even grocery shopping.

Why BNPL Is So Popular

BNPL surged because it solves a few key consumer pain points:

1. Instant approval with low friction

Unlike traditional credit cards, BNPL approvals are almost instant, thanks to automated finance technology systems that evaluate consumer risk in seconds.

2. Predictable payments

Fixed installment schedules make budgeting easier for many shoppers.

3. Zero or low interest

Most BNPL plans offer interest-free payments as long as the user pays on time.

4. Attractive to younger consumers

Gen Z and Millennials, who often avoid credit cards, find BNPL more transparent and easier to manage.

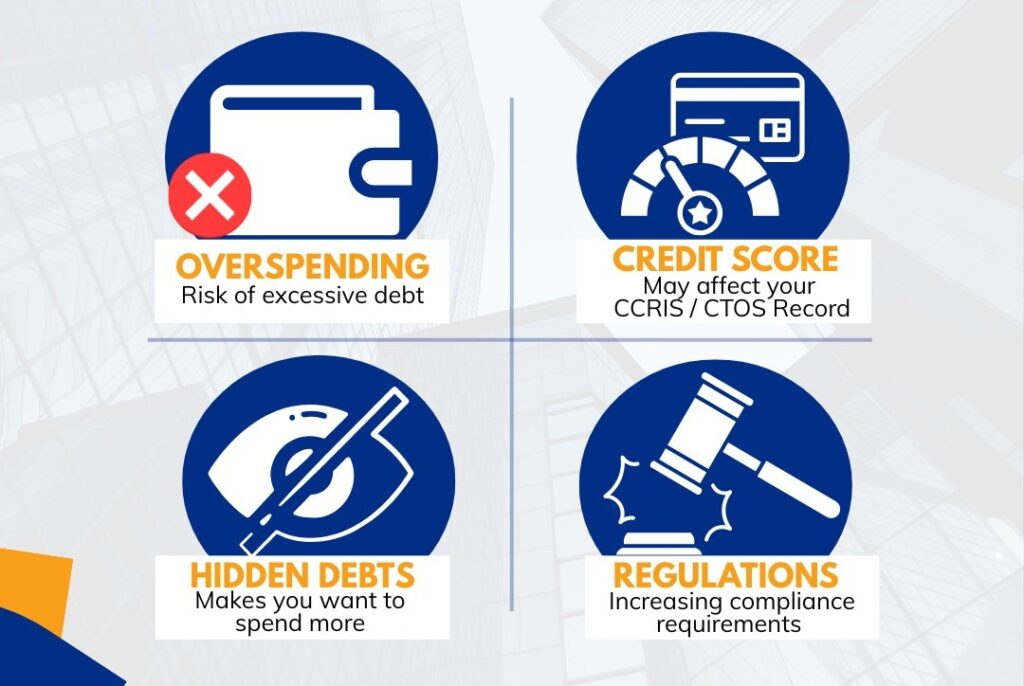

Where BNPL Becomes Risky

Despite the convenience, BNPL is not without downsides. Many consumers underestimate the long-term impact.

1. Encourages overspending

Splitting payments makes purchases appear affordable even when they’re not. Research shows BNPL users spend significantly more than planned.

2. Multiple BNPL loans = hidden debt

Since approvals happen fast and without strict checks, users often take multiple BNPL loans, losing track of repayment dates.

3. Late fees stack up

Missing payments leads to late charges, penalties, and interest turning the “interest-free” model into costly debt.

4. Potential credit score impact

Some BNPL providers report delinquent accounts to credit bureaus, harming credit scores.

5. Limited consumer protection

Unlike credit cards, chargeback protection or fraud coverage may be weaker with certain BNPL platforms.

BNPL’s Role in Modern Finance Technology

BNPL is more than just a payment method it represents how finance technology is changing global consumer behavior.

Key advancements that power BNPL include:

- AI-driven risk scoring

- Real-time payment tracking

- Integration with mobile wallets

- Personalized spending limits

- Merchant-side analytics for dynamic offers

Fintech providers combine automation, data analytics, and user-friendly interfaces to make BNPL feel effortless. However, this same simplicity can sometimes mask the financial risks.

Is BNPL Good or Bad? It Depends.

BNPL Can Be a Convenient Tool When:

- You make payments on time

- You use it for low-value or planned expenses

- You track all active installments

- You avoid stacking multiple loans

BNPL Can Become a Debt Trap When:

- You use it to afford things outside your budget

- You rely on it regularly for essentials (groceries, bills, etc.)

- You lose track of payment dates

- You treat it like “free money”

Ultimately, BNPL is neither good nor bad, it’s a tool. Its value depends on how responsibly it is used.

Tips to Use BNPL Safely

To avoid falling into financial trouble, keep these practices in mind:

- Use only one BNPL provider at a time

- Turn on payment reminders or auto-pay

- Avoid long-term BNPL with high interest

- Don’t use BNPL for luxury or impulse buys

- Review total repayment amounts before agreeing

These small habits protect your financial health while still letting you enjoy the convenience of BNPL.

Final Thoughts

BNPL has become a major force in modern finance technology, offering consumers flexibility and transparency that traditional credit systems often lack. However, its ease of use can also lead to unintentional overspending and silent debt accumulation.

If used thoughtfully, BNPL is a convenient payment solution. If mismanaged, it can quickly evolve into a debt trap.