Insurance plays a major role in financial protection for American households, yet thousands of consumers make costly mistakes every year often without realizing it. Whether it’s health, auto, home, or life insurance, the decisions people make at enrollment or renewal time can affect their long-term financial stability.

Below are the most common insurance mistakes people in the U.S. make, along with practical ways to avoid them.

1. Not Reviewing Coverage Annually

One of the biggest mistakes is failing to update insurance policies. Life changes fast—marriage, divorce, job shifts, a new home, or updated health conditions.

Why it’s a problem

- Outdated policies may not cover current needs.

- You may be paying for coverage you no longer require.

- Missing discounts such as new safety features or improved credit.

How to avoid it

- Set a yearly reminder to review all insurance policies.

- Talk to your agent about changes in income, family size, or property value.

- Compare plans and premiums each year, especially for auto and health insurance.

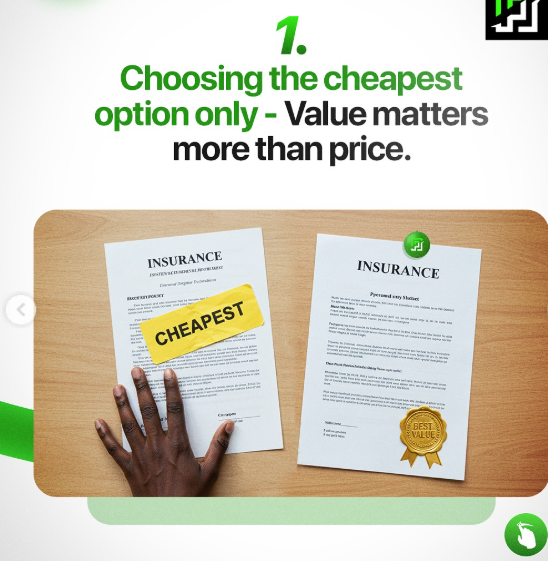

2. Choosing the Cheapest Policy Without Checking Coverage

Many U.S. consumers choose insurance based solely on the lowest premium price.

Why it’s a problem

- Low-cost plans often come with high deductibles.

- Coverage limits may be too low, leaving gaps.

- Important protections (like collision, comprehensive, or supplemental health coverage) may be missing.

How to avoid it

- Compare value, not just cost.

- Check deductibles, exclusions, co-pays, and coverage limits.

- Understand what the plan actually pays for in case of a claim.

3. Underinsuring Home or Auto Assets

People often underestimate the value of belongings, property, or vehicles.

Why it’s a problem

- Homeowners sometimes insure only the market value, not the rebuild cost, which is usually higher.

- Auto owners may skip collision or comprehensive coverage on newer vehicles.

How to avoid it

- Get a professional home replacement-cost analysis.

- Update home inventory lists yearly.

- For autos, keep full coverage until the vehicle’s value drops significantly.

4. Ignoring Deductibles and Out-of-Pocket Costs

Many Americans look only at the premium and forget about how much they’ll pay when filing a claim.

Why it’s a problem

- High-deductible health plans can lead to unexpected medical bills.

- Auto or home insurance claims may require thousands before coverage kicks in.

How to avoid it

- Balance premium vs. deductible based on your savings and risk tolerance.

- If choosing a high-deductible health plan (HDHP), pair it with an HSA (Health Savings Account).

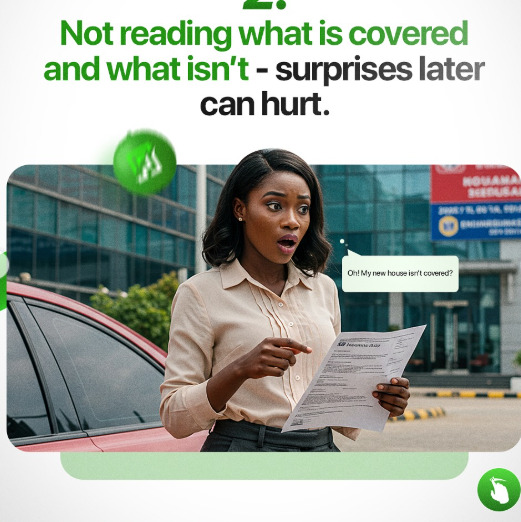

5. Not Understanding Policy Exclusions

Insurance policies in the U.S. often come with detailed exclusions that people rarely read.

Why it’s a problem

- Home insurance may exclude floods, earthquakes, mold, or sewer backups.

- Health insurance may exclude certain treatments or out-of-network care.

- Auto policies may exclude certain drivers or business use.

How to avoid it

- Read the “Exclusions” and “Limitations” sections carefully.

- Ask the agent to explain unclear clauses.

- Buy add-ons (riders) when necessary.

6. Relying Only on Employer Health Insurance

Many people in the U.S. assume employer-sponsored health coverage is always the cheapest and best option.

Why it’s a problem

- Employer plans may have high premiums or limited networks.

- Individual or ACA Marketplace plans can sometimes be cheaper (with subsidies).

- Losing a job can mean sudden loss of coverage.

How to avoid it

- Compare employer coverage with ACA Marketplace options each year.

- Consider supplemental insurance if employer plans seem insufficient.

- Understand COBRA rules before declining other options.

7. Not Buying Enough Life Insurance

Life insurance is often overlooked or purchased at insufficient coverage levels.

Why it’s a problem

- Many Americans rely solely on employer life insurance, which isn’t portable.

- Coverage amounts may not support dependents in long-term needs.

How to avoid it

- Calculate needs based on income, debts, dependents, and future expenses.

- Buy personal coverage separate from employer benefits.

- Review coverage during major life events marriage, kids, buying a home.

8. Failing to Shop Around

Insurance pricing in the U.S. varies widely between companies.

Why it’s a problem

- People pay more simply because they never compare.

- Loyalty doesn’t always mean better rates.

How to avoid it

- Get at least 3–5 quotes before choosing a policy.

- Consider independent agents who compare multiple carriers.

- Re-evaluate pricing every 12 months.

9. Not Disclosing Accurate Information

Some consumers intentionally or unintentionally misrepresent details, such as mileage, health history, or property condition.

Why it’s a problem

- Claims can be denied.

- Policies can be canceled.

- You may face higher premiums later.

How to avoid it

- Provide accurate, updated information at all times.

- Report changes immediately (new drivers, renovations, medical conditions, etc.).

10. Overlooking Discounts and Bundling Options

Insurance companies in the U.S. offer many discounts yet most people don’t take advantage of them.

Common discount opportunities

- Multi-policy bundling

- Good driving behavior

- Safety features at home or in vehicles

- Good credit score

How to avoid it

- Ask for a full list of available discounts.

- Bundle home and auto when cost-effective.

- Improve credit habits, as credit scores affect premiums in many states.

Conclusion

Insurance in the U.S. is complex, and mistakes can become financially draining. However, by reviewing coverage regularly, understanding policy details, comparing options, and being honest with insurers, Americans can protect themselves more effectively.

Avoiding these common mistakes not only leads to smart financial planning but also ensures peace of mind during life’s unexpected events exactly what insurance is meant to provide.